_画板-1-1.png.webp)

By Nicety Machinery Co., Ltd | June 18, 2026

NatureWorks’ Thailand plant represents the most significant capacity expansion in the history of bio-based polymer production — and signals that bioplastics are transitioning from niche to mainstream compounding feedstock.

Overview: Two Materials Segments Outpacing Every Other Polymer Category in 2026

In the global polymer market of 2026 — where the conventional plastics supply chain is under simultaneous pressure from resin price surges, Middle East supply disruption, regulatory mandates, and trade policy distortions — two material categories are consistently outperforming all others in growth rate and investor confidence: bioplastics and elastomers.

The global market for elastomers was valued at $112.7 billion in 2024. The market is projected to grow from $120.4 billion in 2025 to reach $177.7 billion by 2030, at a compound annual growth rate of 8.1% — the highest sustained growth rate of any major polymer segment in the current forecast period. The global bioplastics market volume is reaching 3.3 million metric tons in 2026, from 2.2 million metric tons in 2021, growing at a CAGR of 8.3%.

The practical evidence of these growth trajectories just landed on April 29, 2026: NatureWorks — the world’s leading manufacturer of polylactic acid (PLA) biopolymers — officially opened its new fully integrated Ingeo biopolymer manufacturing facility in Nakhon Sawan Province, Thailand. With 75,000 tonnes of annual production capacity, this is the world’s first second-site integrated PLA plant, making NatureWorks the first PLA producer in history to operate two full-scale manufacturing facilities simultaneously. The $490 million investment — backed by a $350 million loan from Krungthai Bank, one of Thailand’s largest banks — is the largest single capital commitment in the history of commercial biopolymer production.

For plastic compounders, extruder operators, and plant owners, these two developments — the NatureWorks Thailand opening and the elastomers growth surge — define the two fastest-growing material segments that will be entering compounding lines over the next three to five years. Understanding what bio-based polymers and high-performance elastomers demand from processing equipment is becoming commercially essential.

NatureWorks Thailand: The World’s First Second-Site PLA Plant Is Now Open

NatureWorks, the leading manufacturer of polylactic acid (PLA) biopolymers made from renewable resources, announced the grand opening of its new fully integrated Ingeo biopolymer manufacturing facility in Nakhon Sawan, Thailand — 24 years after starting full-scale production at its first manufacturing site in Blair, Nebraska.

The Thailand facility makes NatureWorks the first PLA producer to operate a second production site, adding regional capacity for low-carbon materials used in packaging, fibres, nonwovens, food-service items, consumer goods and 3D printing.

The new site brings together lactic acid production derived from locally sourced sugarcane, lactide monomer production, and polymer manufacturing in a single, fully integrated complex. Located within the Nakhon Sawan BioComplex, the site supports efficient regional supply chains and access to abundant, renewable feedstocks.

The facility has an annual production capacity of approximately 75,000 metric tons of Ingeo biopolymer and is designed to produce the full portfolio of Ingeo grades. Located within the Nakhon Sawan BioComplex, the site supports efficient regional supply chains and access to abundant, renewable feedstocks.

The investment also contributes to regional economic development, creating skilled jobs and supporting local agricultural communities through the sourcing of sugarcane feedstock within a 50-kilometer radius of the production site. By integrating production within the Nakhon Sawan BioComplex, NatureWorks is strengthening partnerships across the local value chain while advancing more sustainable industrial practices.

Erik Ripple, Chief Executive Officer at NatureWorks, said: "With the opening of our Nakhon Sawan facility, we are taking a major step forward in scaling access to Ingeo biopolymers globally. This fully integrated site enables us to better serve our customers while advancing the transition to renewable, lower-impact materials."

Colleen May, President, Cargill Bioindustrials, and Chairperson of the NatureWorks Board, described the opening as "the next chapter in a journey that began decades ago with a simple idea — to create better materials from renewable resources. With this new facility, we are strengthening our ability to scale Ingeo biopolymers globally, while helping our customers meet growing demand for low-carbon solutions."

Narongsak Jivakanun, Chief Executive Officer at GC (PTT Global Chemical, NatureWorks’ Thai shareholder), positioned the investment within the context of global supply chain volatility: "In a highly volatile world, bio-based materials are playing an increasingly important role as solutions that enhance industrial resilience."

That statement — from the CEO of one of Southeast Asia’s largest petrochemical companies — captures the strategic logic driving the bioplastics investment wave in 2026. When fossil-based resin supply chains are disrupted by geopolitical events, hit by tariffs, and constrained by Middle East conflict, a polymer derived from annually renewable sugarcane grown within 50 kilometers of the production facility represents a fundamentally different supply chain risk profile.

What the Nakhon Sawan Plant Produces — and Why It Matters for Compounders

The Nakhon Sawan facility is not simply a PLA pellet plant. It is a fully integrated complex — lactic acid fermentation, lactide monomer production, and PLA polymerization on one site — meaning the entire supply chain from agricultural feedstock to finished biopolymer pellet operates within a single, integrated production system. This integration provides cost efficiency and quality consistency that tolled PLA production from separate suppliers cannot match.

The plant produces the full portfolio of Ingeo grades, including:

Standard Ingeo grades for flexible packaging, rigid thermoformed packaging, compostable food serviceware, and agricultural films — the commodity-volume application categories where PLA is competing head-to-head with conventional PE and PP on both sustainability and, increasingly, performance.

High-heat Ingeo grades — enabled by the melt crystallizer equipment installed at the Nakhon Sawan site, which allows production of crystallized PLA with heat deflection temperatures above 100°C. These grades target hot-fill beverage containers, automotive interior components, and electronics applications where standard amorphous PLA’s relatively low heat deflection temperature of approximately 55°C has been a market limitation.

Ingeo grades for 3D printing filament — one of the highest-volume applications for PLA globally, where NatureWorks’ material consistently dominates the desktop FDM printing market and is gaining share in industrial AM applications.

Nonwoven fiber grades — for hygiene applications including tea bags, coffee capsules, compostable filters, and agricultural nonwovens where PLA fiber is replacing petroleum-based polyester and polypropylene in compostability-specification applications.

For compounders evaluating PLA as a base material for specialty compound development, the Thailand plant’s opening is significant for one practical reason above all: availability. PLA supply has historically been constrained by NatureWorks’ single Nebraska manufacturing site. The addition of 75,000 tonnes of Thai capacity — equivalent to nearly doubling global PLA supply — removes the availability constraint that has prevented many compounders from committing to PLA-based product lines. The next test will be commercial adoption: whether expanded PLA supply can convert sustainability interest into larger-volume substitution in packaging, fibres and consumer applications.

The Elastomers Market Surge: $120 Billion Growing to $177 Billion by 2030

Simultaneously with the bioplastics supply expansion, the global elastomers market is recording its strongest growth trajectory in a decade. The global market for elastomers was valued at $112.7 billion in 2024, projected to grow from $120.4 billion in 2025 to reach $177.7 billion by 2030, at a compound annual growth rate of 8.1%.

This 8.1% CAGR places elastomers ahead of standard engineering plastics (5.4% CAGR), commodity polyolefins (approximately 3–4%), and even the overall plastics market (5.0% CAGR to 2030, per BCC Research’s June 10 market analysis). The elastomers growth trajectory is being driven by the same three end-market forces identified in the HFFR compound article: electric vehicle sealing systems, renewable energy infrastructure (EPDM for wind and solar applications), and AI data center infrastructure requiring specialized elastomeric cable and thermal management components.

But beyond these well-documented demand drivers, 2026 is also seeing elastomers growth from two additional vectors that are less widely discussed:

Medical elastomers. The global medical plastics market is estimated to grow from $31.4 billion in 2024 to $51 billion by 2030, at a CAGR of 10.2%. Silicone, TPE, and specialty rubber grades for medical device components — catheter tubing, syringe seals, respiratory masks, wearable sensor housings — are among the fastest-growing elastomer subcategories. Post-COVID capacity investment in medical manufacturing across Asia has expanded the regional demand base for medical-grade elastomers well beyond what pre-2020 projections anticipated.

Consumer electronics elastomers. The proliferation of wearable devices — smartwatches, fitness trackers, hearables, and the emerging augmented reality headset market — is creating demand for skin-contact elastomers with specific combinations of softness, chemical resistance, colorfastness, and low VOC emission. Silicone and TPU-based elastomers for wearable device bands and housings represent a relatively small but high-margin and fast-growing elastomer application category.

For elastomer compounders, the growth trajectory in volume terms is clear. The margin challenge remains: natural rubber is supply-constrained from Southeast Asian weather disruptions, synthetic rubber (SBR, BR) is 23% above year-ago price levels on butadiene cost pressure, and EPDM feedstock costs remain elevated. Growing into a demand surge while managing elevated raw material costs requires the same operational efficiency discipline that every compounding segment is navigating in 2026.

What Is Driving Bioplastics Demand Beyond Sustainability Marketing

The bioplastics market growth in 2026 is being driven by forces more substantive than brand marketing. Three structural demand drivers are pulling bio-based polymer volumes beyond the sustainability-positioning segment:

Regulatory mandates creating hard demand floors. The EU’s Single Use Plastics Directive and its implementation in member states has created specific application bans — cutlery, plates, straws, stirrers, balloon sticks, and certain food containers — that create hard demand for compostable alternatives in those categories. PLA-based compostable food serviceware is the primary beneficiary. These regulatory demand floors are not discretionary: food service operators in EU member states must use compliant materials or face enforcement.

PCR supply constraints redirecting attention to bio-based alternatives. Plastic recycling is in crisis. Many recycling facilities have shut down globally due to low profit margins, inconsistent feedstock quality, cheap virgin resin pricing, and fluctuating demand. As recycled resin supply becomes unreliable, companies still need to meet sustainability commitments. Bioplastics — especially bio-PE, bio-PP, PLA, and PHA — have become the next viable alternative for brands that cannot source sufficient certified PCR to meet their sustainability targets. The PCR supply shortfall (3.5 million tonnes by 2030, per BKV/Conversio analysis) is functionally increasing demand for bio-based alternatives as a complementary sustainability strategy.

Supply chain resilience as a purchasing criterion. The Middle East conflict’s impact on petrochemical feedstocks — with PE up 50 cents per pound in two months and PP global supply 70% disrupted — has elevated supply chain resilience as an active purchasing criterion for polymer buyers, not just a strategic consideration. Bio-based polymers derived from agricultural feedstocks in politically stable regions (Thailand’s sugarcane, US corn, European sugar beet) offer a diversification of supply chain risk that fossil-based resins derived from Middle Eastern or Russian feedstocks cannot provide. In a highly volatile world, bio-based materials are playing an increasingly important role as solutions that enhance industrial resilience — a statement that is simultaneously a marketing message and a commercially accurate description of the 2026 procurement environment.

Performance parity achieved in key applications. For the first decade of commercial bioplastics, the performance gap between bio-based materials and conventional plastics in most applications was the dominant commercial barrier. That gap has largely closed in the target application categories. PLA’s rigidity, clarity, and compostability make it superior to standard PET in compostable packaging applications — not merely equivalent. High-heat Ingeo grades are now competitive with PS in thermoformed applications requiring moderate heat resistance. Bio-based TPUs are achieving equivalent performance to fossil-based TPUs in most elastomeric film and coating applications.

PLA Compounding: The Processing Challenges That Determine Product Quality

For compounders evaluating PLA as a base material for specialty compound development — impact-modified PLA, nucleated high-heat PLA, PLA/PBAT flexible blends, or fiber-reinforced PLA structural compounds — understanding PLA’s specific processing requirements is essential before investing in line configuration or auxiliary equipment.

PLA is strongly hygroscopic. Ingeo PLA biopolymer absorbs atmospheric moisture rapidly and must be dried to a residual moisture level below 250 ppm (0.025% by weight) before processing. At moisture levels above this threshold, hydrolytic degradation occurs during processing — the ester bonds in the PLA backbone cleave in the presence of water at melt temperatures, reducing molecular weight, decreasing viscosity, and dramatically reducing the mechanical properties of the processed compound. Inadequately dried PLA produces brittle, weak compound regardless of the formulation, and the moisture damage is irreversible — the chain length reduction cannot be recovered by subsequent processing. This makes the pre-processing drying step the single most critical quality gate in PLA compounding.

PLA has a narrow processing temperature window. PLA melts at approximately 170–180°C (Ingeo grade-dependent) and begins thermal degradation above approximately 210°C. This window — roughly 30°C — is significantly narrower than the processing windows for conventional engineering resins like PA66 (melts at 260°C, stable to 290°C) or PC (melts at 240°C, stable to 280°C). Precise extruder temperature profiling, accurate zone-by-zone temperature control, and rapid response to temperature excursions are more critical for PLA processing than for most conventional engineering resins.

PLA is slow to crystallize and requires nucleating agents for high-heat grades. Standard amorphous PLA has a heat deflection temperature of approximately 55°C — adequate for cold-fill packaging and room-temperature consumer goods, but inadequate for hot-fill applications or automotive interior components. Achieving the higher heat deflection temperatures of crystallized PLA (Tg 55°C, Tm 165–175°C) requires either solid-state annealing or the incorporation of nucleating agents that accelerate crystallization kinetics during processing. The uniform dispersion of nucleating agents — typically talc, lactide-based nucleants, or specialized PLA nucleating masterbatches — is a compounding quality variable that directly determines whether the finished compound achieves its target heat deflection temperature.

PLA is shear-sensitive. At high screw speeds or in zones of high screw-specific energy input, PLA can experience localized shear heating that pushes melt temperature above the thermal degradation threshold — producing discoloration, molecular weight reduction, and the characteristic yellowish tint that indicates thermally degraded PLA. Screw design for PLA compounding must balance adequate dispersive mixing for additive incorporation against gentle shear profile to avoid thermal degradation.

PLA blending with flexible polymers for film and packaging applications. One of the most important compounding applications for PLA is blending with PBAT (polybutylene adipate terephthalate) — a petroleum-derived but biodegradable flexible polymer — to produce the PLA/PBAT blends used in compostable flexible packaging and agricultural film. These blends require careful control of blend composition and processing temperature to achieve consistent morphology and the target balance of stiffness and flexibility.

PHA: The Next Biopolymer Wave Entering Compounding Lines

While PLA is the most commercially established biopolymer in compounding today, polyhydroxyalkanoates (PHA) are emerging as the next significant bio-based engineering material category — and several commercial-scale PHA producers are now actively offering material to compounders.

PHAs are produced by bacterial fermentation of organic feedstocks — sugars, fatty acids, or carbon dioxide — and are both bio-based and biodegradable in marine as well as industrial composting environments. This marine biodegradability distinguishes PHA from PLA (which requires industrial composting conditions) and makes it the only bio-based polymer that addresses marine plastic pollution pathways directly.

Bio-based sustainable biopolymers — including PHA — were valued at $2.9 billion in 2025 and are estimated to reach $6.9 billion by 2030, at a compound annual growth rate of 18.8% from 2025 through 2030 — the highest CAGR of any polymer category tracked by BCC Research.

PHA compounding presents different challenges from PLA. PHAs are available in multiple grades — polyhydroxybutyrate (PHB), polyhydroxyvalerate (PHV), and copolymers — with different melting temperatures, crystallization kinetics, and rheological profiles. PHBV copolymers, which are the commercially dominant PHA grades, melt at 140–175°C depending on composition and are relatively brittle without impact modification or blending. PHA compounding for packaging, fiber, and agricultural film applications typically involves blending with other biopolymers — PLA, PBAT — and incorporating nucleating agents and plasticizers to achieve the target balance of stiffness, flexibility, and processing stability.

The compounding challenge with PHA is similar to PLA in moisture sensitivity and narrow processing window, but more acute: PHAs degrade faster than PLA under thermal stress, requiring careful temperature management and rapid processing through the extruder barrel. Residence time management — minimizing the time the polymer spends at melt temperature — is more critical for PHA compounding than for most conventional engineering resins.

Bio-Based Elastomers: The Intersection of Rubber and Renewable Chemistry

The intersection of the bioplastics and elastomers growth trends is bio-based elastomers — a material category that is both growing rapidly and relatively underreported in mainstream plastics industry coverage.

Natural rubber remains the world’s largest bio-based elastomer, with 14 to 15 million tonnes of annual production from Hevea brasiliensis plantations in Southeast Asia. Despite its biological origin, natural rubber faces significant processing challenges in 2026: La Niña-driven disruptions to Southeast Asian tapping operations, concentrated supply in Thailand, Indonesia, and Vietnam, and the sustainability questions around deforestation associated with plantation expansion. These challenges are driving research into alternative natural rubber sources — guayule (a North American desert shrub) and Russian dandelion (Taraxacum koksaghyz) — as well as bio-synthetic alternatives.

Bio-based TPU is one of the fastest-growing bio-based elastomer subcategories. Manufacturers including Covestro (Desmodur eco) and BASF (Elastollan eco) are producing TPU grades based on bio-based diols derived from castor oil, corn, or sugarcane-derived 1,4-butanediol — replacing 30 to 100% of the fossil carbon in conventional TPU with renewable carbon. Bio-based TPU for flexible film, footwear, automotive interior, and wearable device applications is growing at double-digit rates in markets where brand owners have committed to bio-based content targets.

Guayule-derived natural rubber is advancing toward commercial-scale production in the United States and Spain — providing a geographically diversified, domestically grown alternative to Southeast Asian Hevea rubber for automotive seals, medical devices, and specialty elastomeric applications. US government investment in guayule as a strategic domestic rubber supply has intensified following the supply chain disruptions of recent years.

Bio-based EPDM precursors are in advanced development. Conventional EPDM is derived from ethylene, propylene, and a diene monomer (ENB or DCPD) — all fossil-based. Bio-based ethylene (from sugarcane-derived bioethanol) and bio-based propylene (from biorefinery routes) are commercially available in limited volumes and are being evaluated for incorporation into EPDM polymerization, which would give the resulting EPDM a certified bio-based carbon content — attractive for automotive and wind energy customers with renewable content targets.

The Future of BioPlastics 2026 Conference: Next Week’s Industry Agenda

For compounders and processing professionals wanting to engage directly with the bioplastics and bio-based elastomers technology landscape, the most immediate opportunity is the Future of BioPlastics 2026 (FoB:Plast 2026) conference, taking place online on June 24–25, 2026 — just six days from now.

The event focuses on bioplastics and bio-based materials and explores how sustainable plastic solutions can become both economically viable and market-ready. Central topics include innovative materials, new applications, scaling and commercial implementation, as well as regulation, recyclability, and circular economy strategies. The event is designed for startups, SMEs, large companies, research institutions, investors, and policy stakeholders across the bio-based plastics value chain.

For compounders specifically, the most valuable sessions at FoB:Plast 2026 will be those addressing the practical barriers to commercial bio-based compound production: cost competitiveness versus fossil-based alternatives, processing equipment compatibility, certification and compostability labeling requirements, and end-of-life pathway documentation for PPWR compliance. The NatureWorks Thailand opening is expected to generate significant conference discussion — the availability of 75,000 additional tonnes of PLA per year changes the commercial calculus for compounders evaluating bio-based product lines.

What Compounders Should Prepare for as Bio-Based Polymers Enter Their Lines

For compounders currently processing only conventional fossil-based engineering resins who are evaluating bio-based polymer processing for the first time — or who are receiving customer inquiries about bio-based compound availability — the key preparation actions are:

1. Characterize your drying system performance against bio-based polymer requirements. PLA requires drying below 250 ppm moisture, which is more stringent than most conventional engineering resins. PHA requires even more careful moisture management with tighter temperature control during drying to avoid thermal degradation in the dryer itself. Verify that your existing drying equipment can achieve and hold the bio-polymer specification before committing to a bio-based compound line.

2. Assess your extruder’s temperature zone accuracy for narrow-window processing. PLA’s 30°C processing window requires barrel zone temperature accuracy of ±2°C or better across all barrel zones. If your existing twin-screw or single-screw extruder has older PID controllers with slow response times, upgrading the temperature control system is likely the most cost-effective pre-investment before commissioning a bio-polymer compound line.

3. Plan for nucleating agent and plasticizer incorporation infrastructure. Nucleating agents and impact modifiers for PLA — and blending components like PBAT for flexible compound grades — require consistent pre-blending and dosing infrastructure upstream of the extruder. Retrofitting accurate gravimetric feeding and high-shear pre-blending capability to an existing line that was not configured for multi-component additive incorporation is a common and correctible investment gap.

4. Evaluate your post-pelletizing moisture management infrastructure. PLA and PHA pellets will reabsorb atmospheric moisture from the moment they exit the cooling water bath. Post-pelletizing centrifugal drying, followed by desiccant air-drying of the pellet stream before packaging, is the correct infrastructure for bio-polymer compound lines — particularly in humid production environments where moisture reabsorption rates are high.

5. Contact NatureWorks about Ingeo availability from the Thailand plant. With the Thailand facility now operational, Asia-Pacific compounders have direct access to Ingeo supply from regional production for the first time. Lead times, minimum order quantities, and grade availability from the Thailand site should be confirmed directly with NatureWorks’ Asia-Pacific commercial team.

Equipment for Precise, Quality-Consistent Bio-Based Polymer Processing

Bio-based polymers — PLA, PHA, bio-based TPU, and bio-based elastomers — impose more demanding requirements on the auxiliary equipment chain than conventional engineering resins, primarily because of their moisture sensitivity, narrow processing temperature windows, and sensitivity to shear-induced thermal degradation. The right equipment configuration is the difference between a bio-polymer compound line that produces consistent, specification-compliant output and one that generates off-spec product from batch to batch due to inadequate moisture control or mixing inconsistency.

Mixing — Precision Pre-Blending for Temperature-Sensitive Bio-Polymers

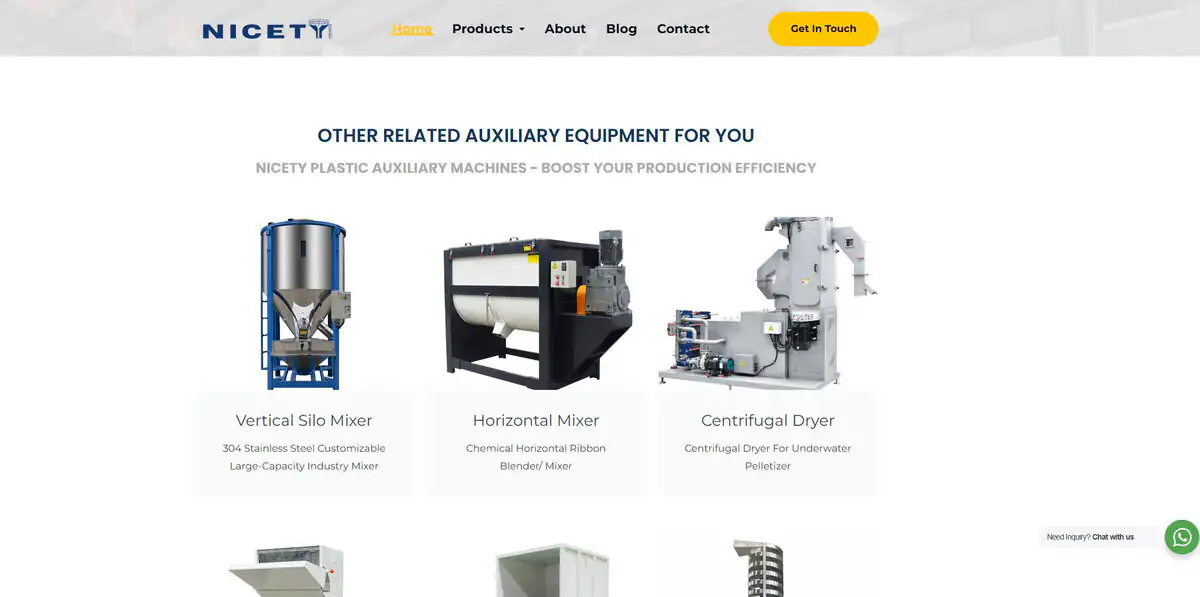

Nicety Machinery’s plastic mixer range provides the precision pre-blending capability that bio-based polymer compounding requires — while delivering the temperature control discipline that PLA and PHA’s narrow processing windows demand.

The High Speed Mixer Machine pre-blends nucleating agents, impact modifiers, plasticizers, and functional additives into PLA or PHA base resin before extrusion — achieving the uniform additive distribution that determines whether the finished compound hits its target heat deflection temperature, impact performance, and optical properties. For PLA/PBAT flexible blend compounds, the high speed mixer pre-coats PLA pellets with the PBAT content and compatibilizer package, ensuring the blend enters the extruder with the pre-dispersion needed for consistent morphology development during extrusion. The temperature control of the mixing cycle is critical for PLA: the hot-mix temperature must be sufficient to activate coupling agents and surface-treat filler particles, but must not exceed the PLA softening point — a requirement that distinguishes PLA mixing from conventional engineering resin mixing.

The Horizontal Mixer handles bulk pellet-to-pellet blending — mixing PLA pellets with PBAT, masterbatch, or other blend component pellets at defined ratios before the extruder feed. For bio-polymer compound lines producing multiple grades, the horizontal mixer provides consistent blend composition across production batches without the risk of stratification that gravity-fed blending can produce.

The Plastic Color Mixer handles precision let-down of nucleating agent masterbatch, colorant, and functional additive concentrates at defined ratios — ensuring that each batch of bio-polymer compound contains the exact additive dosage required to meet heat deflection, compostability certification, and optical specification targets.

The Vertical Silo Mixer homogenizes PLA pellet batches from multiple deliveries in the storage silo — smoothing any molecular weight variation between Ingeo production lots before the material enters the compounding extruder. For compounders sourcing PLA from both the Blair, Nebraska and Nakhon Sawan, Thailand production sites simultaneously — which will be an option from 2026 — silo-level homogenization protects compound consistency across sourcing variations.

VOC Deodorizing Drying — The Most Critical Equipment for Bio-Polymer Quality

The VOC Deodorizing Drying System is the single most important auxiliary equipment investment for any bio-polymer compounding line. Its criticality for PLA and PHA processing goes beyond what conventional engineering resin drying requires — for three specific reasons:

Ultra-low moisture specification. PLA must be dried below 250 ppm moisture before processing — a specification more demanding than PA66 (typically 200 ppm) and far more demanding than PC (typically 500 ppm) or PP (essentially moisture-insensitive). The VOC Deodorizing Drying System’s desiccant-based moisture removal capability achieves and holds the sub-250 ppm specification consistently across continuous production, including in the high-humidity environments of Southeast Asian manufacturing plants where NatureWorks’ Thailand production will be consumed regionally.

Temperature-controlled drying to prevent thermal pre-degradation. PLA cannot be dried at the high temperatures used for PA or PC. Drying temperatures for PLA are typically limited to 80–90°C maximum to prevent chain scission in the dryer itself — before the material even reaches the extruder. The VOC Deodorizing Drying System’s precise temperature control across the drying bed prevents over-temperature exposure that would degrade PLA molecular weight before processing, protecting the compound quality that the extruder and formulation can then deliver.

VOC removal for bio-based lactic acid residues. Ingeo PLA contains trace lactic acid and lactide oligomer residues from the polymerization process that volatilize during thermal processing — generating characteristic odor that is particularly sensitive in food contact and consumer goods applications. The VOC deodorizing function removes these residues from the pellet surface and interstitial voids before processing, improving the odor profile of finished PLA compound and reducing VOC emission during the customer’s injection molding or extrusion step — a specification requirement for automotive interior and food contact PLA compound grades.

Centrifugal Drying — Surface Moisture Removal Before Thermal Drying

The Strand Line Centrifugal Dryer removes surface water from PLA and bio-polymer compound pellets mechanically — immediately after the water-bath cooling step — before hygroscopic PLA pellets can reabsorb moisture from ambient air during the interval between strand cooling and the downstream VOC Deodorizing Drying System.

The importance of centrifugal drying for PLA compounding lines is amplified compared to conventional engineering resin lines for one reason: PLA’s moisture reabsorption rate from the pellet surface is faster than most conventional engineering resins, particularly in warm, humid environments. In a tropical production environment — Thailand, India, Southeast Asia generally — the humidity gradient between the cooling water bath and ambient air creates a rapid moisture reabsorption driving force that the centrifugal dryer must neutralize. Reducing pellet surface moisture to near-zero at the centrifugal dryer stage before the pellets move to the thermal drying stage is the equipment sequence that protects PLA pellet quality in challenging ambient conditions.

Vibrating Spiral Elevator — Gentle Elevation for Fragile Bio-Polymer Pellets

The Vibrating Spiral Elevator provides gentle height transition for PLA and bio-based elastomer compound pellets between the pelletizer or centrifugal dryer and the downstream screening and drying stages.

Bio-polymer compound pellets — particularly PLA-based compounds that have not been nucleated to high crystallinity — are mechanically more fragile than conventional engineering resin pellets at room temperature. Their lower flexural modulus and brittleness make them more susceptible to chipping, fracturing, and fines generation under mechanical impact than glass-filled PA or PC pellets. The vibrating spiral elevator’s gentle vibratory conveying mechanism — moving pellets upward through a helical track without the impact loading of belt conveyors or the high-velocity friction of pneumatic systems — protects bio-polymer pellet integrity through the final stages of the production line, preventing the fines generation that creates feeding problems at the customer’s injection molding or extrusion machine and that degrades the surface aesthetics of finished bio-polymer products.

For compact plant layouts where the vibrating spiral’s footprint is constrained, the Z Elevator provides an alternative inclined conveying path for bio-polymer pellets between process stages — enclosed and gentle, protecting moisture-sensitive PLA and PHA pellets from re-humidification during height transitions.

Post-Pelletizing Size Classification

The Linear Vibrating Screener classifies bio-polymer compound pellets to the dimensional specification required by injection molding and extrusion customers — removing fines and oversized pellets before packaging. For certified compostable PLA compound grades — where product certification (EN 13432, ASTM D6400) requires consistent material properties across the supply chain — pellet size consistency is part of the quality declaration that supports the compostability claim. The screener is the equipment that enforces this consistency at the production output stage, protecting the integrity of the certified bio-polymer compound brand from batch to batch.

Sources

- Business Wire / NatureWorks: Grand Opening of Fully Integrated Ingeo Biopolymer Manufacturing Facility in Thailand — April 29, 2026

- Plastics News: NatureWorks Opens Thailand PLA Plant, Expanding Global Bioplastics Capacity — April 29, 2026

- AlchemPro: NatureWorks Opens New PLA Biopolymer Plant in Thailand — April 30, 2026

- TEXtalks: NatureWorks Opens Thailand Ingeo Plant, Expanding Global PLA Supply — May 6, 2026

- BCC Research / GlobeNewsWire: Global Plastics Market to Reach $197.8 Billion by 2030 — June 10, 2026

- BCC Research: Global Elastomers Market $120.4 Billion in 2025, Growing to $177.7 Billion by 2030, CAGR 8.1% — December 2025

- BCC Research: Global Bio-Based Sustainable Biopolymers Market $2.9 Billion 2025, CAGR 18.8% to $6.9 Billion by 2030

- NatureWorks Official Press Release: Ingeo PLA Manufacturing Expansion — Krungthai Bank $350M Financing

- PTT Global Chemical: NatureWorks’ Ingeo PLA Manufacturing Expansion — Partnership with Cargill and GC

- Future of BioPlastics 2026 Conference: June 24–25, 2026 — Online Event, Green Chemistry for Sustainability

- Plastics Staffing: Will Bioplastics Go Mainstream in 2026? — December 2025

- SkyQuestT: Global Engineering Plastics Market $112.57 Billion in 2024, CAGR 5.4% to 2033

- Plastics News Sustainable Plastics: Latest Industry Developments — June 2026

_画板-1-副本-3-pxeey2xejyohpkvf07tglhvew6ks2ts3pjvhagm60c.png.webp "NICETY MACHINERY Co., LTD")