_画板-1-1.png.webp)

By Nicety Machinery Co., Ltd | May 30, 2026

Compounding plant operators in rubber, engineering plastics, and recycled polymers are navigating the most punishing cost environment in years — squeezed simultaneously from raw material, feedstock, regulatory, and trade dimensions. Photo: Unsplash

Overview: The Squeeze That Is Different From Every Previous Cycle

Plant owners and operators running compounding facilities for rubber, engineering plastics, or recycled polymers in 2026 are navigating a cost environment that is structurally different from previous price cycles — and more dangerous. It is not a single commodity moving. It is not a temporary logistics disruption. It is a simultaneous convergence of raw material cost surges, regulatory cost mandates, trade policy distortions, and supply chain restructuring that is hitting every segment of the compounding industry at the same time, from different directions, with no obvious short-term resolution.

Synthetic rubber prices as of May 29, 2026 stand at 14,758 CNY per tonne — still 23.33% higher than a year ago, despite a 9.74% monthly pullback from recent peaks. Post-consumer recycled (PCR) resin currently costs approximately one-third more than equivalent virgin resin — meaning the regulatory mandate to use more recycled material is simultaneously a mandate to absorb higher input costs. Polyethylene settled 30 cents per pound higher in April contracts, with LyondellBasell nominating a further 20 cents for May. Polypropylene is described by LyondellBasell as the "sleeping giant" of the current surge, with 70% of global virgin PP supply disrupted. And the tariff structure that was designed to encourage domestic production is, in practice, making cheaply imported PCR resin more attractive than domestically produced recycled material — undermining the recycling infrastructure that compounders are being asked to use.

No segment of the compounding industry is untouched. This article is written specifically for the plant owners and operators who need to understand what is happening, why it is happening, and what operational decisions are available to them right now.

Rubber Plant Owners: Synthetic Rubber 23% Higher Year-on-Year Right Now

For operators of rubber compounding plants — mixing SBR, BR, EPDM, NBR, IIR, or CR-based compounds for tire, automotive, industrial, or consumer applications — the headline number is stark. As of May 29, 2026, synthetic rubber is trading at 14,758 CNY per tonne, which is 23.33% higher than the equivalent date one year ago. The recent monthly pullback of 9.74% from peak levels does not change the structural picture: rubber compounders are operating with a raw material cost base that is substantially elevated compared to 2025 budgets, on a sustained basis.

The immediate cause of the synthetic rubber price surge is a compounding (no pun intended) of multiple feedstock and supply disruptions. Natural rubber — the base against which synthetic rubber pricing is always partially benchmarked — entered 2026 in what analysts are describing as a structural squeeze rather than a cyclical spike. The La Niña weather pattern brought unseasonable rainfall to Thailand and Vietnam throughout late 2025, severely hampering rubber tapping activities just as the industry entered the 2026 low-production window. Natural rubber futures stabilized at levels not seen in years following this disruption.

The synthetic rubber market, rather than absorbing overflow demand from constrained natural rubber supply, is simultaneously facing its own feedstock pressures. The traditional "synthetic fallback" — switching compounding recipes toward synthetic rubber grades when natural rubber becomes expensive — is proving less effective than in previous cycles. With synthetic rubber prices also elevated on energy and feedstock costs, the substitution that previously provided a safety valve no longer dampens price volatility for compounders caught between both markets.

For rubber compounding plant owners, this means every batch of compound produced in 2026 is being produced at a materially higher raw material cost than was anticipated in capital investment decisions made 18 to 36 months ago. The question is not whether margins are compressed — they are. The question is which operational levers are available to recover some of that compression without losing customer relationships or market position.

The Butadiene Problem: Why SBR and BR Compounders Have No Easy Exit

Within the synthetic rubber market, the most acute cost pressure is in styrene-butadiene rubber (SBR) and polybutadiene rubber (BR) — the two dominant synthetic rubber grades in tire and automotive rubber compounding. Both are derived from butadiene, a C4 hydrocarbon byproduct of steam cracking of naphtha or ethane.

Spot butadiene in Asia climbed 67% from 2024 to 2025 on cracker outages, squeezing emulsion-SBR margins when tire makers resisted price hikes. Solution-grade plants — which produce the functionalized S-SBR grades required for modern high-performance tire compounds — faced additional cost pressures, with purity premiums of USD 100 to 150 per tonne eroding their cost advantage over emulsion grades.

The butadiene shortage is not a simple logistics problem that resolves when shipping normalizes. It is a production problem: butadiene availability is structurally linked to steam cracker operating rates, which in turn are driven by ethylene production economics. When ethylene margins are weak — as they have been in the current oversupplied petrochemical cycle — crackers reduce operating rates, and butadiene availability tightens as a byproduct. The Middle East supply disruption affecting polyolefin feedstocks is adding further complexity to C4 stream availability globally.

For SBR and BR compounders, there is no easy exit. Switching to alternative elastomers — EPDM, NBR, or specialty grades — requires customer requalification that takes months, and not all applications can substitute elastomer types without fundamental performance compromise. The operational response must therefore focus on processing efficiency: getting more usable compound from each kilogram of expensive SBR or BR rather than seeking material substitution.

The EPDM Opportunity Inside the Crisis

While SBR and BR compounders are most acutely exposed to the butadiene cost surge, EPDM compounders are seeing a different dynamic — one that creates genuine market opportunity alongside cost pressure.

EPDM is projected to expand at a 5.81% CAGR through 2031, driven by roofing and automotive weatherstrip upgrades, wind turbine seal and gasket requirements for offshore and onshore installations, and the expanding electric vehicle market. Wind turbine nacelles cycle between −40°C and +60°C, requiring EPDM seals with ozone and UV resistance that no other cost-competitive elastomer provides at that temperature range. As renewable energy infrastructure buildout accelerates globally, EPDM demand from this sector alone is creating meaningful volume growth.

For EPDM compounding plant operators, the current environment is therefore a two-sided story: ethylene-propylene feedstock cost pressure on the input side, but genuinely growing end-market demand in roofing, EV weatherstripping, and wind energy seals on the output side. Compounders who can maintain quality consistency and reliable delivery schedules through the current cost cycle will be positioned to capture contract gains as the EPDM demand surge continues. This is precisely the environment where production line efficiency determines which compounders gain share and which lose it.

Engineering Plastics Compounders: Five Resins Moving Up Simultaneously

For compounders processing engineering thermoplastics — PA6, PA66, PC, ABS, PBT, and their glass-filled, flame-retardant, and impact-modified derivatives — the 2026 cost environment is the most broadly synchronized upward move in years.

Polyethylene settled 30 cents per pound higher in April contracts alone, with an additional 20 cents per pound nominated for May — a potential cumulative increase of 50 cents per pound in two months. Polypropylene is being called the "sleeping giant" of the current surge, with approximately 70% of global virgin PP supply affected by Middle East feedstock disruption versus around 20% for PE. PA6 and PA66 face price-hike nominations of 5 to 12 cents per pound going into Q2, with the Lone Star dual acquisition of RadiciGroup and DOMO Engineered Materials adding a structural dimension to PA66 pricing as two of Europe’s largest PA compounders consolidate under single ownership. ABS pricing is moving on benzene and butadiene cost support — benzene has crossed USD 4 per gallon, and butadiene (the same feedstock squeezing SBR compounders) is also the feedstock for the rubber phase in ABS.

The consequence for engineering plastics compounding plant owners is the same as for rubber operators, but potentially more acute: engineering compound customers — automotive Tier 1 suppliers, electronics manufacturers, appliance OEMs — have multi-quarter contract cycles that lag resin market movements. A compounder buying resin on monthly contracts and selling compound on quarterly contracts absorbs the full cost increase for one to two full working capital cycles before pricing recovery is possible.

The Lone Star/RadiciGroup/DOMO consolidation also signals a structural trend that plant owners should watch: as engineering plastics compounder capacity consolidates into larger, vertically integrated entities with own polymer production, smaller independent compounders lose the option to play suppliers against each other. The procurement leverage that existed when RadiciGroup and DOMO competed for the same customers is diminishing as they come under unified ownership.

Recycled Plastics Plant Owners: The Counterintuitive Trap — PCR Costs More Than Virgin

Of all the paradoxes facing compounding plant owners in 2026, the most damaging for the recycled plastics sector is also the most counterintuitive: post-consumer recycled (PCR) resin currently costs approximately one-third more than equivalent virgin polymer.

This is not a temporary market distortion. It is a structural economics problem: PCR production lacks the economies of scale present in virgin resin manufacturing, which benefits from decades of process optimization, massive throughput, and vertically integrated feedstock supply chains. The cost base for producing high-quality recycled plastics is higher than virgin plastic production at equivalent scale — and that cost differential is passed through to buyers.

The consequence is a regulatory trap. The EU PPWR, five US states’ PCR content mandates, and brand owner sustainability commitments are all pushing compounders toward incorporating more PCR into their compounds. But incorporating more PCR means accepting a raw material that costs 30% more than the virgin equivalent — and doing so while simultaneously managing the quality variability, moisture content, VOC loading, and processing challenges that PCR feedstock introduces. The sustainability mandate is simultaneously a cost mandate and a process complexity mandate.

For recycled plastics compounding plant owners who built their business model on the assumption that PCR pricing would converge toward virgin pricing as scale developed, 2026 has been a reckoning. Recyclers who went bankrupt in recent years — Umincorp, TRH, Ecocircle, Ioniqa, and Alpek’s Pennsylvania PET recycling facility — are data points in a pattern of fragile economics meeting market reality. Planned chemical recycling investments by petrochemical players are being delayed. The recycling infrastructure that sustainability strategies depend on is contracting rather than expanding in the near term.

The Tariff Distortion: Imported PCR Is Cheaper Than Domestic, Destroying Domestic Recyclers

The tariff environment in 2026 was designed to favor domestic production. For recycled plastics, it is producing the opposite effect — and it is one of the most practically damaging issues facing domestic PCR compounders and recyclers right now.

Virgin resin imports attract a 15% global tariff, making imported virgin resin more expensive and theoretically favoring domestic PCR as a substitute. But PCR imports are not subject to equivalent tariff treatment — and consumer brands facing cost pressure are turning to cheaper imported recycled resin rather than paying a premium for domestically produced PCR. Tariff uncertainty, strained consumer spending, and the cost difference between international and American material all factored into a soft and unstable U.S. postconsumer resin market in 2025, with conditions expected to continue in 2026.

The Association of Plastic Recyclers describes this as a "perfect storm of problems arising all at the same time." Consumer brands have pulled back on ambitious voluntary PCR targets but are still using recycled resin — they depend on cheaper imports, which may not be certified as post-consumer material or may originate in countries without equivalent environmental and labor standards.

For domestic PCR compounders, the situation is existential: they are being asked to invest in quality, certification, and traceability systems to meet brand owner sustainability requirements — while competing against cheaper, less-scrutinized imported PCR that brand owners are buying instead because it hits the sustainability label while costing less. This is not a sustainable competitive environment for domestic recyclers and recycled-content compounders, and the closure of multiple recycling plants in 2025 and 2026 reflects that reality.

The 3.5 Million Tonne Gap: Why PCR Supply Cannot Meet Regulatory Demand by 2030

The quantitative dimension of the PCR supply problem is now well-documented. By 2030, EU regulatory demand for recycled plastic content across packaging, automotive, and industrial applications is anticipated to reach 13 million tonnes. Under a conservative business-as-usual scenario, the supply shortfall is 3.5 million tonnes. Even under an ambitious advanced scenario accounting for significant investments in both mechanical and chemical recycling, a gap of 788,000 tonnes remains.

In Germany alone, the supply shortfall under conservative assumptions ranges between 310,000 and 861,000 tonnes — a country with among the most developed recycling infrastructure in the world.

Chemical recycling plants take approximately three years to build, meaning new facilities must begin construction by 2027 to contribute meaningfully before 2030. The European Commission’s February 2026 ratification of updated rules covering chemically recycled content in PET beverage bottles opens the door to wider commercialization — but regulatory clarity on chemical recycling’s contribution to PPWR compliance targets is still developing, and the energy intensity of pyrolysis-based chemical recycling compared to mechanical recycling remains a concern.

For compounding plant owners building their product roadmaps around PCR-containing grades, the supply shortage signal is important: the feedstock they will need to meet regulatory requirements is in structural short supply relative to the demand that regulations will create. This is an argument for securing long-term PCR supply agreements now — before the regulatory demand ramp hits — rather than relying on spot market procurement.

What All Three Types of Compounding Plants Have in Common Right Now

Rubber, engineering plastics, and recycled plastics compounders are facing different specific pressures — but they share a common operational reality in 2026 that defines what effective management looks like:

Raw material cost is no longer the only variable to optimize. When a single resin or rubber grade represents 60 to 80% of a compound’s cost, and that material has moved 20 to 30% higher in a matter of months, the traditional procurement focus on price negotiation is necessary but insufficient. The efficiency with which that expensive raw material is converted into saleable compound — yield, rework rate, reject rate, energy per kilogram — becomes a cost variable of equivalent importance.

Customer pricing lags raw material reality. Across all three segments, compound buyers are on quarterly or semi-annual pricing cycles that do not adjust immediately to monthly resin market movements. Compounders are carrying the cost difference in working capital while waiting for contract adjustments. This makes operating cash flow management, not just margin management, a critical near-term priority.

Processing quality is a cost variable, not just a quality variable. In a high-raw-material-cost environment, every kilogram of off-spec compound that requires rework or disposal represents an amplified loss. The processes that determine first-pass compound quality — pre-blending consistency, drying adequacy, dispersion uniformity, pellet size classification — have a direct and measurable cost impact when input materials are priced at 2026 levels.

Feedstock diversification is now a risk management function, not a procurement convenience. Single-source dependency on any one resin, rubber grade, or PCR stream is a structural vulnerability in the current environment. Qualifying alternate suppliers and maintaining the flexibility to process multiple feedstock sources — without line performance degradation — is a competitive requirement.

The Processing Efficiency Imperative: Nine Operational Actions for Plant Owners

Based on the cost pressures across all three compounding segments, these are the nine highest-impact operational actions available to plant owners right now:

1. Audit first-pass yield by product line. Calculate the actual yield rate — kilograms of saleable compound produced per kilogram of raw material consumed — for each compound grade. In a high-raw-material-cost environment, a yield improvement of 1 to 2 percentage points has a direct P&L impact that can be calculated at current resin prices.

2. Tighten pre-blending process control. Most compound quality failures originate at the pre-blending stage — inconsistent additive distribution, inadequate dispersion of fillers, uneven masterbatch let-down. Tightening the mixing step before the extruder or internal mixer directly reduces downstream reject rates.

3. Review drying protocols for all hygroscopic feedstocks. PA6, PA66, PC, PBT, and PCR feedstocks all require controlled drying before processing. Inadequate drying produces hydrolytic degradation in engineering resins and quality inconsistency in PCR compounds. Validating drying system performance — temperature, residence time, dew point — and re-certifying drying equipment against actual feedstock moisture specifications is a direct quality protection action.

4. Validate all additive loadings against current application requirements. Carbon black loadings, glass fiber levels, flame retardant dosages, and stabilizer packages set in lower-cost environments may be carrying safety margins above minimum application specification. A structured formulation audit can identify legitimate loading reductions — validated by mechanical and functional testing — that reduce additive cost without compromising customer compliance.

5. Accelerate alternate feedstock qualification. For every key raw material — including rubber grades, engineering resins, PCR streams, and additives — identify and begin qualifying at least one alternate approved source. The current environment makes single-source supply an unacceptable operational risk.

6. Implement or tighten pellet size classification. Post-pelletizing screening is the last quality gate before product ships to customers. Off-spec pellets that reach customers generate returns, replacements, and potential qualification losses that cost significantly more than the rework cost of catching them internally.

7. Review energy consumption per kilogram of output. Energy represents 20 to 30% of total production cost in most compounding operations. Extruder screw speed optimization for specific energy consumption (SEC) per kilogram — rather than maximum throughput — reduces energy cost per unit while also reducing shear-induced degradation that increases reject rates.

8. Secure PCR supply with long-term agreements now. For compounders with regulatory mandates driving PCR content requirements, the 3.5 million tonne EU supply shortfall projected for 2030 is a forward procurement problem that begins now. Long-term contracts at current pricing lock in PCR availability before regulatory demand pushes supply tighter.

9. Review contract structures for price escalation mechanisms. Fixed quarterly compound pricing is a liability in a market where key input costs move monthly. Floating pricing mechanisms tied to published resin or rubber price indices — ICIS, Platts, or SHFE benchmarks — provide cost recovery structure that fixed contracts cannot.

Equipment That Pays Back Faster in a High-Cost Input Environment

In a market where rubber is 23% higher year-on-year, PE is up 50 cents per pound in two months, and PCR costs more than virgin, the financial return on equipment that improves processing yield and reduces material waste accelerates proportionally with input cost levels. Equipment that had a 3-year payback at 2024 raw material prices may have an 18-month payback at current 2026 prices — because every kilogram of waste it prevents represents a larger monetary loss than it did 18 months ago.

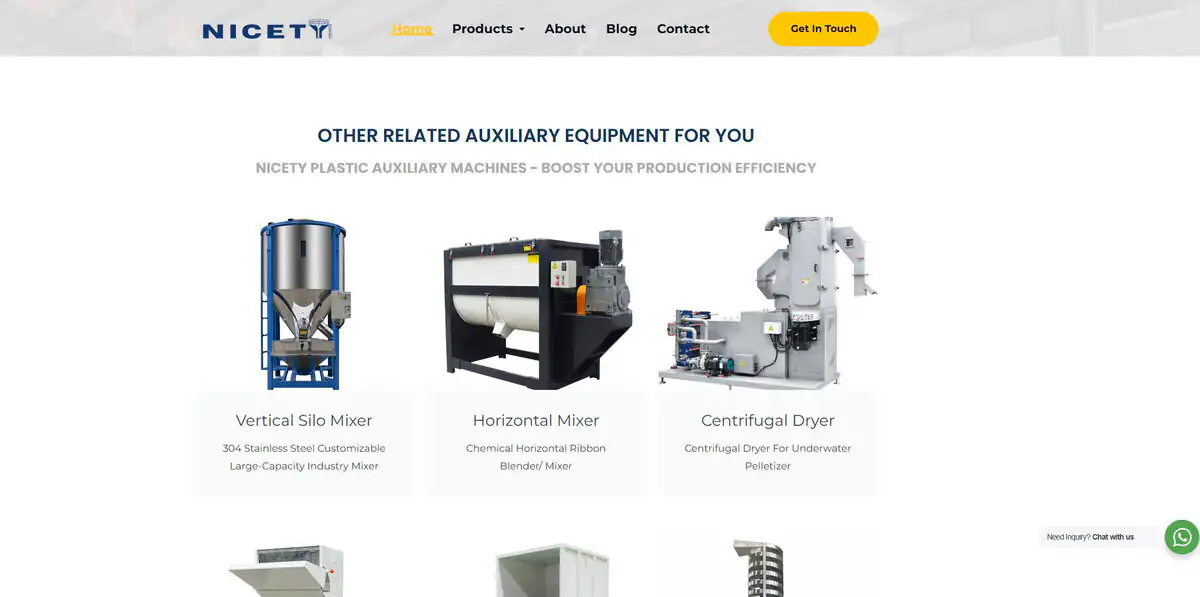

High-shear pre-blending for rubber and engineering plastic compounds: The High Speed Mixer Machine provides the critical pre-dispersion step before the internal mixer or twin-screw extruder — breaking up filler agglomerates, uniformly coating rubber or resin particles with processing aids and stabilizers, and ensuring the additive distribution that determines compound consistency and reject rate. For rubber compounders incorporating expensive carbon black, silica, or specialty fillers into SBR, EPDM, or NBR compounds, pre-blending quality directly determines how much of those expensive additives ends up in saleable product versus off-spec rework.

Precision masterbatch and colorant let-down: For engineering plastic compounders, precise additive dosing at the pre-blending stage prevents over-addition of costly masterbatches, flame retardants, or stabilizers. The Plastic Color Mixer delivers accurate, repeatable let-down ratios — preventing both quality failures from under-dosing and material waste from over-dosing at current additive prices.

Consistent bulk blending for PCR-virgin mixes: Facilities incorporating PCR content into engineering plastic or polyolefin compounds need reliable pellet-to-pellet blending that maintains the certified PCR content ratio across every batch — both for compound quality and for regulatory compliance documentation. The Horizontal Mixer and Vertical Silo Mixer provide consistent bulk blending of pellets with different densities and morphologies, preventing the stratification between PCR and virgin pellets that undermines blend uniformity and certification accuracy.

Segregation-free conveying of pre-blended materials: Moving pre-blended rubber or plastic compound mixes from the mixing stage to the processing machine without disrupting blend homogeneity is essential — particularly for PCR blends where density differences between recycled and virgin pellets create segregation risk. The Screw Conveyor and Vibrating Spiral Elevator provide gentle, consistent material transfer that preserves the blend quality achieved at the mixing stage through to the extruder or internal mixer feed point.

Drying and VOC removal for PCR and hygroscopic engineering resins: PCR feedstocks carry elevated moisture and volatile organic compound loads compared to virgin resin. Engineering resins — PA, PC, PBT — are hygroscopic and require controlled drying to prevent hydrolytic degradation. Processing either category of material without adequate pre-treatment produces degraded compound that wastes expensive input material and generates rejects. The VOC Deodorizing Drying System handles both moisture removal and VOC reduction before processing — protecting compound quality and ensuring food-contact compliance for PCR-containing packaging compounds.

Post-extrusion pelletizing and size classification: The Extrusion Pelletizing Line converts compound melt into uniform pellets. The Strand Line Centrifugal Dryer removes surface moisture immediately after the water-bath cooling step. The Linear Vibrating Screener then classifies pellets to specification — removing fines and oversized material before packaging. In the current raw material cost environment, the screener is the last line of defence against shipping off-spec product that generates customer returns — which means replacing expensive compound at today’s prices, not the prices when the production budget was set.

Z elevator for compact plant layouts: For compounding facilities with constrained floor space where height transitions between process stages are unavoidable, the Z Elevator provides reliable inclined conveying of pellets or granular material between stages without the segregation risks of pneumatic conveying — critical for PCR blends and abrasive glass-filled engineering compounds.

The operational message for 2026 is consistent across rubber, engineering plastics, and recycled polymer compounding: the cost environment has raised the stakes for every process decision. Equipment that prevents waste, improves yield, and maintains consistency is not a capital expenditure to be deferred — it is a cost recovery mechanism with accelerated payback at current input prices.

Sources

- Trading Economics: Synthetic Rubber Price — May 29, 2026 Live Data (14,758 CNY/T, +23.33% YoY)

- Bright Rubber Plastic: 2026 — The Rubber Market’s Structural Squeeze — March 2026

- CAPMAD Agribusiness: Global Rubber Shortage — Prices Could Soar in 2026 — January 2026

- Mordor Intelligence: Synthetic Rubber Market — Butadiene +67%, S-SBR EV Transition, EPDM 5.81% CAGR 2026–2031

- Resource Recycling: Five Trends Shaping PCR Packaging to 2031 — April 29, 2026

- Resource Recycling: How Will 2026 Unfold for Plastics Recycling? — February 2026

- Packaging Dive: Plastic Scrap Imports Add to "Perfect Storm" Hitting Domestic PCR — January 29, 2026

- Waste Management World: PCR Supply Shortfall 3.5 Million Tonnes by 2030 — BKV/Conversio Study

- Simon-Kucher: Navigating Challenges and Opportunities in the Plastic Recycling Market — December 2024

- Plastics Technology: May 2026 — Price Trajectory for All Resins Shifts Sharply Upward

- LyondellBasell Q1 2026 Earnings Call: PP "Sleeping Giant," 70% of Global Supply Disrupted — May 1, 2026

- Extera: Plastics Industry Outlook Q1 & Q2 2026 — Recycling Infrastructure Contracting

- Cornerstone Management: How 2026 US Tariffs Could Affect Plastic Manufacturing Costs — December 2025

_画板-1-副本-3-pxeey2xejyohpkvf07tglhvew6ks2ts3pjvhagm60c.png.webp "NICETY MACHINERY Co., LTD")