_画板-1-1.png.webp)

By Nicety Machinery Co., Ltd | May 16, 2026

Every major resin category is moving sharply upward in May 2026 — and compounders absorb the blow first.

Overview: The Most Synchronized Resin Price Surge in Years

In May 2026, plastic compounders and extruder operators across North America, Europe, and Asia are absorbing what multiple market analysts are describing as the most broadly synchronized upward pressure across resin categories that many buyers have seen in several years. Every major commodity resin — polyethylene, polypropylene, PVC, polystyrene, ABS, and the principal engineering thermoplastics — has moved sharply higher since March, driven by the ongoing Strait of Hormuz supply disruption, a 15% global tariff on imported resin feedstocks and finished resins, planned and unplanned production outages, and surging export demand pulling North American supply into international markets faster than domestic output can replenish it.

For compounders who buy base resin and sell finished compound, this is a margin event with no buffer. Downstream customers want pricing held; upstream suppliers are enforcing increases. The compounding step sits between them, and the equipment running those lines — twin-screw extruders, pelletizers, and the full auxiliary equipment chain — determines whether each kilogram of expensive resin produces saleable product or costly rework.

The Numbers: Where Each Resin Stands as of Mid-May

The scale and speed of price movement in 2026 is exceptional across the full resin portfolio:

Polyethylene (PE): US April contracts settled higher by 30 cents per pound compared to March. LyondellBasell has nominated an additional 20 cents per pound increase for May volumes — a potential cumulative increase of 50 cents per pound, or approximately USD $1,102 per metric ton, in just two months. LyondellBasell CEO Peter Vanacker noted that "four weeks ago, nobody expected or predicted that we would get a 30 cent per pound price increase for polyethylene." In Europe, PE price increases reached EUR 200 to 500 per tonne. In India, cumulative increases hit INR 35,000 to 50,000 per metric ton depending on grade.

Polypropylene (PP): US virgin PP prices have increased by 25 to 35 cents per pound since March. In Europe and Asia, they have risen by 35 to 55 cents per pound — a steeper move than PE in those regions. LyondellBasell, during its May 1 earnings call, called PP a "sleeping giant," explaining that approximately 70% of global virgin PP capacity is affected by the Iran war, versus around 20% of virgin PE capacity. PP price increase potential ahead may exceed what PE has already delivered.

Engineering resins: ABS prices, flat through most of Q1 2026, are now moving as feedstock benzene crossed $4 per gallon and butadiene moved sharply higher. PA6 and PA66 — already under cost pressure from the Lone Star/Radici/DOMO consolidation disruption — face additional input cost pressure. PET paraxylene feedstock settled at its highest April level in years, with two major producers implementing increases effective immediately, skipping standard contract timing. PC pricing, previously buffered by Chinese supply overhang, is beginning to move on genuine feedstock cost support.

PVC: Ethylene firmed in March and April, directly supporting increases across the PVC chain. The VYNOVA Wilhelmshaven insolvency and Runcorn administration have tightened European S-PVC availability simultaneously with input cost increases — a double squeeze for European PVC compounders.

PE: The 30-Cent Shock and the May Nominations That Followed

The polyethylene price surge is the anchor story of the 2026 resin market. The mechanism is straightforward: approximately 50% of global polyethylene capacity is either directly offline or indirectly constrained through feedstock shortages tied to the Strait of Hormuz disruption, according to assessments from BIC Advisory Group and Dow CEO Jim Fitterling.

International buyers — unable to source from the Middle East and facing constrained Asian supply as Asian refiners cut operating rates, shut units, and declare force majeure — have turned aggressively toward North America. Michael Greenberg, CEO of Resintel, described the dynamic: "Buyers who delayed purchases earlier in the cycle were forced back into the market at higher numbers, and availability remained nearly as important as price."

That export demand pull is tightening domestic US availability even where domestic end-use demand — in automotive, housing, and appliances — would not otherwise justify current price levels. Producers are running assets at higher rates to capture the margin opportunity. LyondellBasell is ramping up run rates for its North American assets, including Dow’s new Freeport, Texas plant. But supply cannot recover fast enough to moderate prices materially through Q2.

LyondellBasell’s position is that the company does not expect a sharp decline in polyethylene prices in the second half of 2026, citing ongoing supply disruptions — a notably bearish statement for downstream buyers in compound and extrusion businesses planning H2 purchases.

PP: The Sleeping Giant That Is Now Fully Awake

While PE grabbed headlines first, polypropylene is now the more structurally exposed material. LyondellBasell’s Kim Foley, Executive Vice President of Olefins and Polymers, explained why during the May 1 earnings call: unlike polyethylene, polypropylene is typically consumed close to where it is produced. North America is historically a net importer of PP. When Asian producers lose access to feedstock propane — as is happening now, with multiple propylene dehydrogenation (PDH) units offline — Asian PP supply contracts without a natural North American export alternative to replace it.

Foley said LyondellBasell expects North America to shift from net importer to net exporter of PP, as international buyers seek North American supply to replace lost Asian volumes. That structural shift, if it materializes, would pull US PP supply into export channels and further tighten domestic availability for US and Mexican compounders and extruder operators who depend on domestic PP pricing.

For compounders running PP-based compounds — glass-filled automotive grades, impact-modified packaging compounds, TPO blends — the PP story is now more serious than PE. The 70% global supply disruption figure carries a much longer recovery tail than the PE market’s 50%.

Engineering Resins: ABS, PA, PC, PVC All Moving Together

What makes May 2026 different from previous price shock cycles is the breadth of the move. It is not one resin — it is every resin. For compounders who process engineering thermoplastics alongside polyolefins, there is no safe harbor in the portfolio.

ABS pricing is moving on both butadiene and styrene cost support — the two monomers that together with acrylonitrile define the ABS cost structure. Benzene, the feedstock for styrene, has crossed $4 per gallon. Butadiene has moved sharply higher. Automotive ABS demand remains soft, which gives buyers some negotiating room — but the feedstock mathematics are real, and producers have documented cost grounds for the increases they are nominating.

Nylon 6 (PA6) prices faced price-hike nominations of 5 to 12 cents per pound going into Q2 from suppliers seeking to recover margin lost in late 2025. The Lone Star dual acquisition of RadiciGroup and DOMO Engineered Materials — consolidating the two largest European PA compounders — adds a structural dimension to PA66 pricing that could reduce competitive pressure on prices even after the feedstock cycle stabilizes.

Polycarbonate (PC) pricing is stabilizing at a higher base after dropping 10 to 15% in Q4 2025. Chinese supply overhang, which previously capped any PC price recovery, is now being offset by genuine feedstock cost increases on the BPA chain.

For compounders processing PVC, the supply side is deteriorating simultaneously with input cost increases. European S-PVC availability has tightened due to the VYNOVA Wilhelmshaven insolvency and Runcorn administration, while ethylene costs are firming. PVC compounders in Europe face both a supply and a cost problem.

The Tariff Layer on Top of the Supply Shock

The price shock from Middle East supply disruption is being compounded by a 15% global tariff that continues to apply to imported resin feedstocks and finished resins. According to Resin Technology Inc., the tariff effectively maintains a significant duty on imported polymers, which limits downward price flexibility even in situations where domestic supply might otherwise moderate.

Compounders who import specific resin grades — certain PA66 grades sourced from Europe, specialty engineering resins with limited domestic production, or recycled polymer content sourced internationally — face the tariff cost on top of underlying commodity price increases.

In Southeast Asia, domestic polymer prices rose 50% to 100% during March and April 2026 in some cases, prompting policy responses in import-dependent economies struggling with inflationary pressure from rising resin costs. For compounders in Asia supplying global customers, the margin compression is acute: resin cost doubles while export pricing negotiations with Western customers remain anchored to pre-crisis baselines.

Why Compounders Get Squeezed First and Hardest

In a resin price surge, the plastics compounding step absorbs the worst of the margin compression. The reason is structural.

A resin producer passes costs forward within weeks — producers like LyondellBasell implement increases on rolling 30-day contract cycles. A downstream injection molder or extruder passes costs forward on quarterly contract reviews with their OEM customers, with typical adjustment cycles of 60 to 90 days. The compounder sits in the middle: buying resin on the same 30-day cycles as everyone else, but selling compound on contracts negotiated with downstream processors who are themselves in cost-recovery mode and unwilling to absorb full pass-through.

The working capital consequence compounds the problem. A compounder buying 30-day resin contracts and selling 60 to 90-day compound contracts carries the cost increase in inventory for one to two full working capital cycles before pricing can be adjusted. With PE up 30 cents per pound on a 90-day lag, a mid-size compounder processing 1,000 metric tons per month faces a margin bridge of approximately USD $330,000 before pricing adjusts.

The only structural response available within the compounding operation itself — beyond procurement and pricing negotiations — is to reduce the cost of processing each kilogram of resin that does come through the door.

Six Operational Levers Compounders Can Pull Right Now

When resin costs surge simultaneously across the full portfolio, the compounding operation itself becomes a cost management tool. These are the six levers with the most immediate impact:

1. Yield optimization above all else. Every percentage point of off-spec product — compound that must be reground, reprocessed, or scrapped — wastes resin that now costs significantly more than it did 90 days ago. Tightening process control on the mixing and extrusion step, reducing agglomeration and poor dispersion that cause rejects, and improving first-pass yield are the highest-leverage actions available.

2. Pre-blending consistency. Inconsistent additive dispersion entering the extruder — uneven glass fiber distribution, agglomerated flame retardant particles, non-uniform masterbatch let-down — causes localized formulation variation that shows up as off-spec compound at the pellet screening stage. Improving pre-blending homogeneity before the extruder is the upstream fix for downstream waste.

3. Extruder energy efficiency. Energy costs account for 20 to 30% of total production costs in compounding. When resin costs surge, energy efficiency becomes relatively more valuable as a margin lever. Running extruders at optimized screw speeds for specific energy consumption (SEC) per kilogram — rather than at maximum throughput — reduces energy cost per kg while also reducing shear-induced degradation that increases rejects.

4. Formulation review for additive loading. Carbon black loadings, glass fiber levels, and flame-retardant dosages set in lower-cost environments may be running at conservative safety margins above minimum specification. A structured formulation audit — validating actual performance against application requirement, not original target — can identify legitimate opportunities to reduce expensive additive loading without compromising customer specification compliance.

5. Procurement diversification and qualification. Compounders with single-source resin supply are fully exposed to each producer’s price nomination. Those with alternate qualified sources have negotiating leverage and supply security. The current price environment is the right moment to accelerate qualification of alternative suppliers for key resin grades — even if the alternate is not the preferred choice in normal conditions.

6. Contract structure negotiation. Monthly fixed-price contracts are now the most dangerous contract structure a compounder can hold on the buy side. Floating contracts with defined feedstock-referenced escalation mechanisms — tied to published ethylene, propylene, or benzene contract indices — are more manageable when costs are rising at the current rate. This is a legitimate subject for renegotiation even mid-contract.

Processing Equipment That Pays for Itself Faster When Resin Costs Rise

In a high resin-cost environment, every piece of auxiliary equipment that improves yield, reduces rework, or prevents material degradation generates measurable return — measurable in current resin prices, not the prices of 12 months ago.

Pre-blending and additive dispersion before the extruder: The High Speed Mixer Machine is the most impactful equipment upgrade available for compounders experiencing high reject rates from poor additive dispersion. High-shear pre-blending breaks additive agglomerates and coats resin pellets or powder uniformly before the extruder — reducing the dispersion demand on the screw and lowering the rate of off-spec output per kilogram of expensive base resin. For color mixing and masterbatch let-down, the Plastic Color Mixer delivers precise, repeatable blend ratios that prevent over-dosage of costly colorant concentrates.

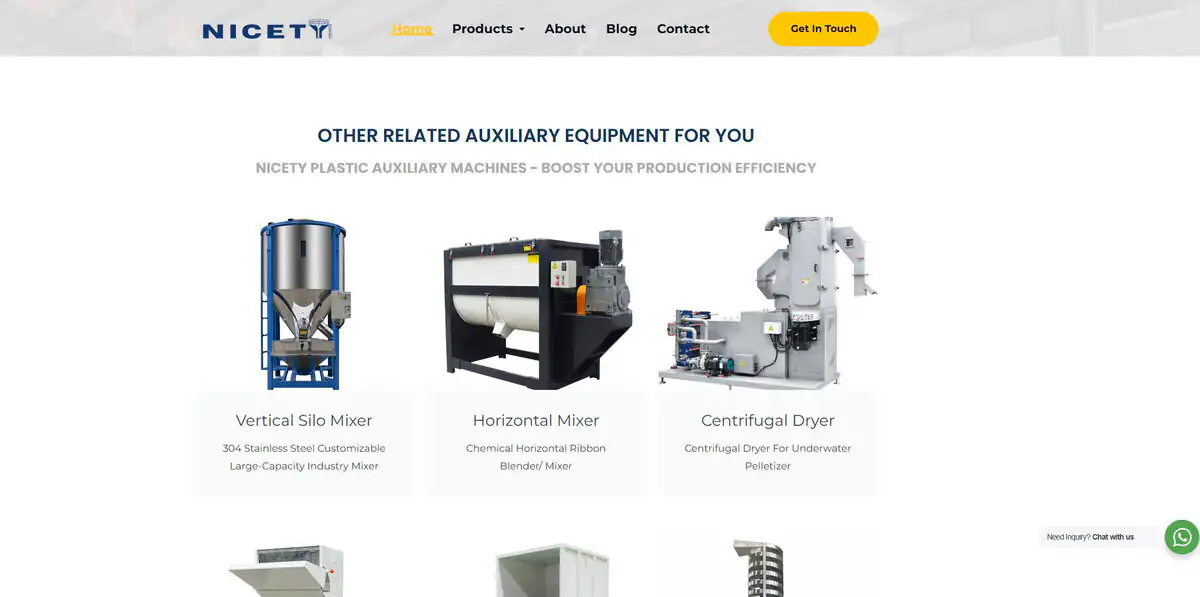

Homogeneous bulk blending for pellet-to-pellet mixing: When blending pre-compounded pellets, regrind, or multiple resin grades into a single feed stream, the Horizontal Mixer and Vertical Silo Mixer prevent stratification and segregation that lead to inconsistent extruder feed — and inconsistent compound output. Batch-to-batch formulation consistency is a direct yield variable.

Conveying without segregation or degradation: Moving pre-blended materials from mixing equipment to the extruder hopper without breaking up the blend — or introducing fines and contamination — protects the mixing work done upstream. The Screw Conveyor and Vibrating Spiral Elevator move materials gently and consistently, preserving blend quality through to the extrusion step.

Moisture and VOC control before processing: Hygroscopic resins — PA6, PA66, PBT, PC — processed with inadequate drying produce hydrolytically degraded compound with reduced molecular weight and mechanical property loss. Every kilogram of degraded compound is a kilogram of now-expensive resin converted to off-spec material. The VOC Deodorizing Drying System manages both moisture removal and volatile organic compound reduction before the extrusion step, protecting compound quality across the engineering resin range.

Post-extrusion pelletizing consistency: The Extrusion Pelletizing Line converts compound melt into uniform pellets, and pellet uniformity is a direct quality variable for downstream molders and extruders. Inconsistent pellet size leads to customer returns — which in the current price environment means absorbing the cost of replacing expensive resin compound at today’s prices. The Strand Line Centrifugal Dryer removes surface moisture from pellets immediately after water-bath cooling, preventing moisture reabsorption into hygroscopic engineering resins and protecting pellet quality through to packaging.

Screening and quality separation: The Linear Vibrating Screener removes fines and oversized pellets before packaging — preventing off-spec material from reaching customers. In a market where resin costs are up 30 to 50% in two months, catching and reworking an off-spec batch before it ships is significantly cheaper than replacing it after a customer return.

Sources

- Plastics Technology: May 2026 — Price Trajectory for All Resins Shifts Sharply Upward

- Resource Recycling: LyondellBasell Sees Upside for PP Over PE — May 8, 2026

- Resource Recycling: PP Most Likely Plastic to Shift in 2026 — May 8, 2026

- Plastics News: LyondellBasell Sees Prolonged PE Supply Shock — May 1, 2026

- Plastics News: LyondellBasell Expects PE Prices to Stay High Through 2026

- Plastics Today: From Hormuz to Resin — How the Iran Conflict Is Resetting Polymer Pricing

- Plastics Today: Resin Price Report — Feedstock Costs Just Reset the Plastic Resin Market — April 2026

- Plastics Today: Resin Pricing Shifts Amid Feedstock Volatility

- Argus Media: LyondellBasell Seeks 35¢/lb Hike for US PE Through May — March 2026

- Syntex America: Hormuz Crisis Week 3 — 50% of Global PE Supply Disrupted — March 2026

- Plastics Today: Updated 2026 Insider’s Guide to Resin Pricing

- Investing.com: JPMorgan Raises LyondellBasell Stock Price Target on Polyethylene Gains

_画板-1-副本-3-pxeey2xejyohpkvf07tglhvew6ks2ts3pjvhagm60c.png.webp "NICETY MACHINERY Co., LTD")